Expansions spur trading, both prior to realease and after. The effect of the preparation for Retribution can best be seen in the Mineral Price Index, which rose by 8% from October to November. A rise was to be expected, as Retribution brought new Tech I ships and major changes to many of the already existing Tech I ships.

Nocxium, Isogen and Zydrine prices contributed most to the rise in the MPI. The prices of these three minerals rose by 17%, 20% and 26% respectively. The price of Morphite rose by 33% in the period, even though it is not used in the production of the new or modified ships. On the other hand, the prices of Tritanium, Pyerite and Mexallon were very lightly affected. Only Isogen and Morphite show a notable increase in traded volume between months. The increase is 17% for Isogen and 20% for Nocxium. Traded volume of other minerals remains stable or even falls, as is the case for Zydrine and Megacyte.

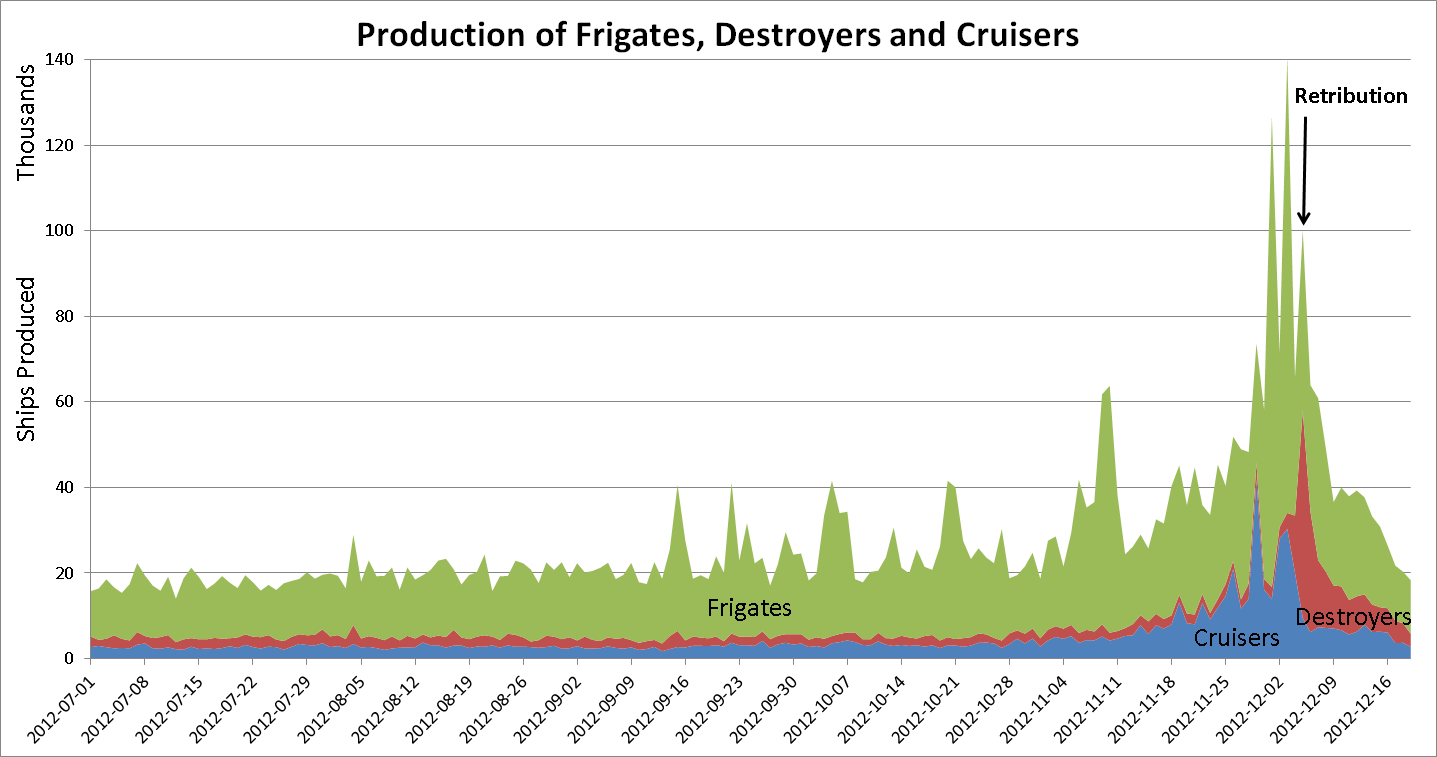

The following graph shows how Retribution affected the manufacturing of frigates, destroyers and cruisers.

There may have been less hoarding of minerals than one might have expected prior to this expansion. There was, however, some discussion among traders about the announced changes to NPC supplied containers, which are now made by players. There was the possibility that the new player-made containers would be recyclable, making it possible for industrialists to gain vast quantities of minerals from local NPC supply, thus saving on transportation hassle. Given enough material requirements, the recycled materials might even have become much cheaper than market prices. Pilots may remember a similar incident from the introduction of Planetary Interaction.

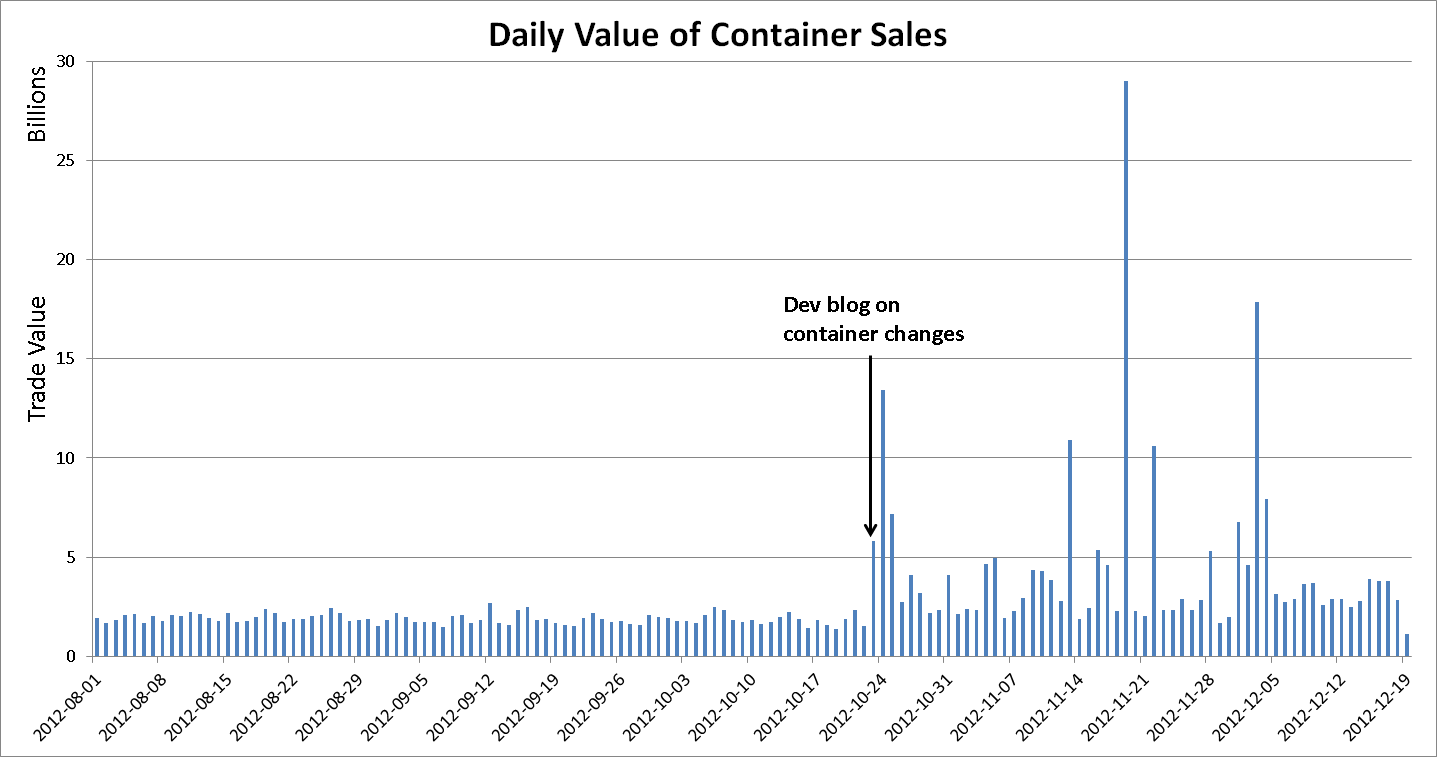

The following graph shows the trade in containers.

The data shows some large but isolated spikes in container sales but not an all out frenzy. Total container sales in October and November were only 86% above the total sales value for August and September. It‘s heartwarming to see that the majority of players did not risk their money on CCP repeating the mistake from the introduction of Planetary Interaction. However, there were a few that did. The biggest single buyer of containers in the period from the dev blog announcement to deployment bought containers for 28 billion ISK. There‘s a good chance there‘s a station out there somewhere where you can get a good price on containers on the secondary market.

The index values for November are:

|

|

November 2012 |

1 Month Change |

12 Month Change |

|

Mineral Price Index |

130.6 |

8.1% |

68.5% |

|

Primary Producer Price Index |

84.9 |

-1.7% |

3.0% |

|

Secondary Producer Price Index |

108.2 |

-0.6% |

-5.6% |

|

Consumer Price Index |

81.8 |

0.7% |

14.6% |

Changes in the Mineral Price Index have already been covered. The Primary Producer Price Index showed a 1.7% deflation, driven by datacores supplied from Factional Warfare, while the Secondary Producer Price Index saw 0.6% deflation, with hardly any changes of note. The Consumer Price Index displayed 0.7% inflation, with most categories changing very little. Most of the inflation is caused by an 11% rise in implant prices, which has to do with loyalty points being a bit harder to come by in Factional Warfare.

All in all, this was fairly quiet month on the markets, except for the mineral market. The figures for December will obviously be less stable and the effect of the rising mineral prices and increased activity should become clearly visible as inflation in consumer prices.

For more detail on the indices, please refer to the Market Indices page on Evelopedia.

Full series of the four main price indices in Excel format.

Full series of the four main price indices in CSV format.